Up Home

Up grew faster than any other neobank in Australia or overseas – almost entirely on customer referrals. By 2023 Up’s NPS was a staggering 51.5% (Roy Morgan), we had the #1 most satisfied digital bank customers (Canstar) and the #1 rated banking app in both the Google Play and Apple App stores.

That reputation, and the relatively tiny cost of growth that it made possible, put us in an interesting position when choosing how to monetise.

Credit cards were completely off the table: our core value was helping young Australians learn to save, not get them into consumer debt. My newsletter was all about putting together emergency funds, saving for the first time, or keeping your money together when you have mental health challenges. We’d gone out with major white hat PR campaigns attacking Buy Now Pay Later and the damage that repackaged credit does to young Australians just getting started with money management. Our strong values made brand partnerships delicate, and usually not profitable!

We had no regrets, but a simple fact was that many, if not most of the ways that banks in Australia make money were automatically off the table. We wanted our first step to monetisation to be something that:

Would make us financially viable long term and

Actually helped our customers.

A number of options were tabled - an ethical home loan was quickly picked as the clear winner. For the bank, and for our ‘Upsiders’, many of whom dreamed of home ownership but assumed it was way out of reach.

Take a First Step: Home Savers

Every savings dream starts with a dollar. We wanted to start Upsiders off with a very simple, but special, savings account.

Home Savers are free. On the bank side, they act like any other kind of savings account, but the experience for customers is special. You can input your dream home price, then see how much your real deposit is (minus costs like stamp duty) and play visual games to play with how long it will take you to get to auction day with your current, or a different savings path.

That’s obviously helpful for Upsiders. For us - this helps identify intent. Though we knew that - since our customers are mostly under 35 - many would not yet be ready to buy, we had indicators of intent and a way to track whether our efforts to help educate and encourage customers were working. A good conversation at the Board level and a great health indicator for the future.

Learning-Free Learning

Buying a home is one of the biggest learning curves life can throw at you. What’s the difference between offset and redraw? Why is it so hard to get a loan on a tiny apartment? What the heck is a boardroom auction, what do you mean I have to pay $700 for a building and pest when I might not even buy it and omg, I want to curl up in a ball already.

We wanted to help Upsiders learn how to ‘do’ home loans, well before they were ready to actually buy - so that when the time came they’d feel empowered. But sticking them in a classroom wasn’t an option. So I designed a short, snackable, and actually fun in-app content series.

Over the program’s first year, 97% of users rated the educational content useful and so many asked us to make the content available to their mates, that we moved some of it online too: here are some favourites.

Plain English Guide to Home Loan Words

Plus, I got to write about how important it is to scope out the local chicken shop before you buy your first home. The ultimate win-win-win.

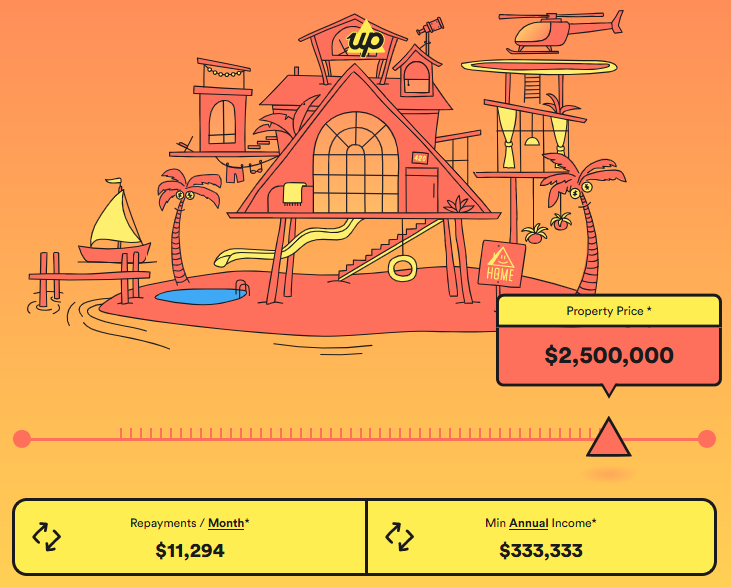

A home loan calculator, but eeeasy.

Any home loan marketing team will tell you that their calculator is a core marketing tool. Whether it’s gated or not, customers will play with calculators over and over again, potentially for years.

The issue for us was designing a calculator that made sense for our customers and our product. Most calculators are complex, and not built with first homeowners in mind. They’re very useful if you’re experienced, but can also be totally overwhelming. And it’s hard to find one that takes the entire experience into account, including things like stamp duty.

We took a look at what matters most to new buyers, and made a new kind of tool that presents only an answer to their essential question: what could I buy and what would the loan cost?

Plus, we made it really, really fun to use. Click here and scroll down for the whole experience, helipads and all.

Welcome Home.

Part of the Up Home welcome pack - click through to see the whole merch experience.

Every housewarming deserves a gift. Up merch is always top notch quality and.. very bright! We sent every Up Home customer the kind of gift box that would get guests asking… what on earth is that??

No media spend. Just results.

Up Home was the best kind of product launch: no ATL spend, no media budget, no aggressive SEM. This was a product launch, and a product, couched in genuine relevance and ease: no scammy subtext, no extra fees, just a great experience Upsiders love and recommend.

In Home Savers’ first year more than 16,000 unique Upsiders created a Home Saver, and 10,000+ were still actively saving at the end of that year. The following year, 1000 new-to-bank loans were issued for Up Home, despite an intimidating financial climate for first home buyers.

People who made this possible:

The tiny-but-brilliant Up marketing team: Paul Tagell, Seb Neylan, Ruki Da Silva and developer Andy Carson (builder of the Up Home calculator).

Design: Sometimes in a writer’s life, they’re lucky enough to pair with the kind of designer who challenges you, lifts your words and makes the whole thing sing - that’s Sharma Heylen-Silvia.

And on the product side - too many awesome folk to mention, but - Justin French and Sunni Cooper are the people you need when the dream is ‘turn this impossibly difficult and regulated product into something lovable’ or ‘hey guys I just rewrote the terms and conditions because I hate the language, can you OK that’?’